Brian Bongard REALTOR®

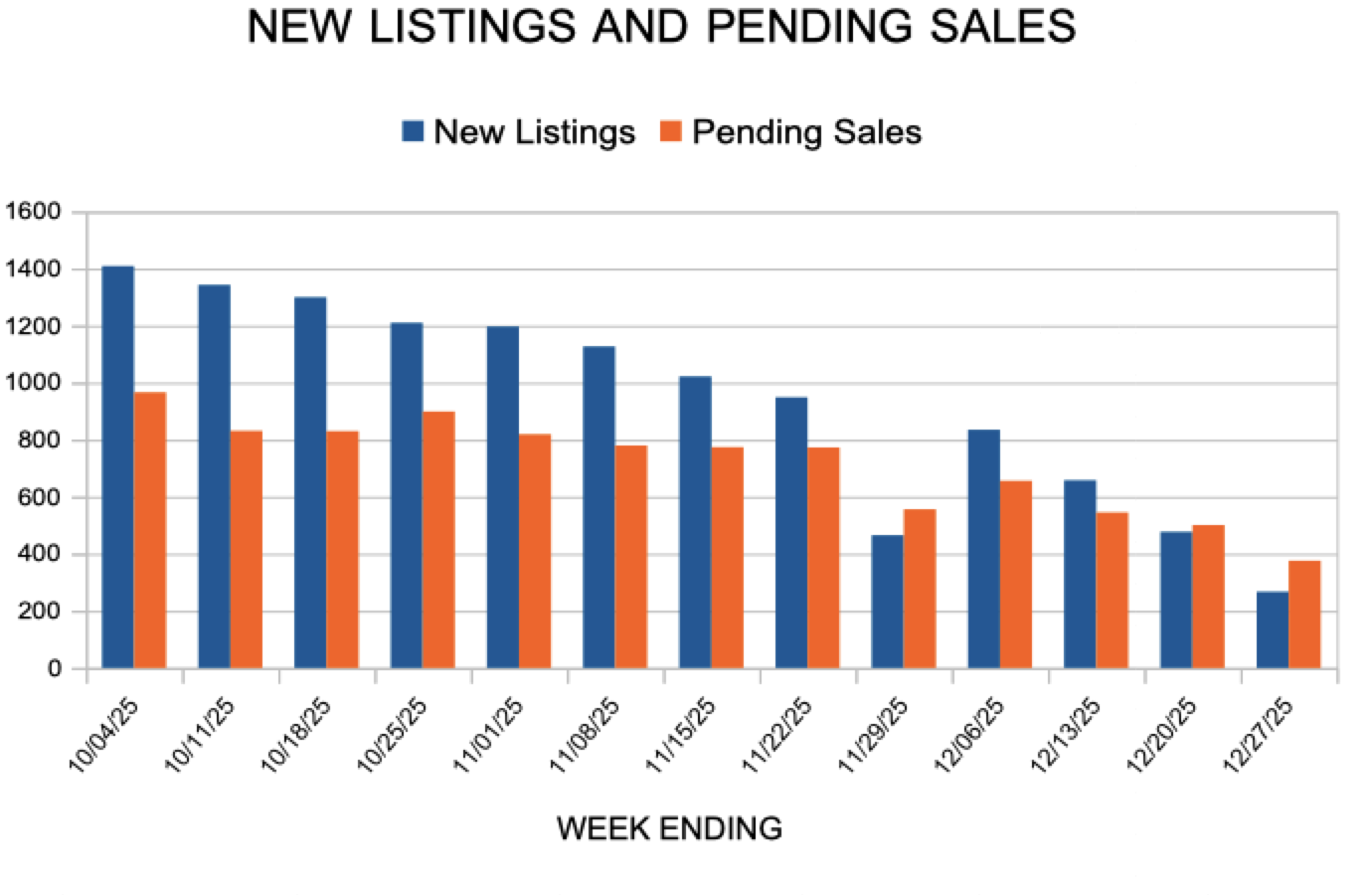

January 12, 2026 by

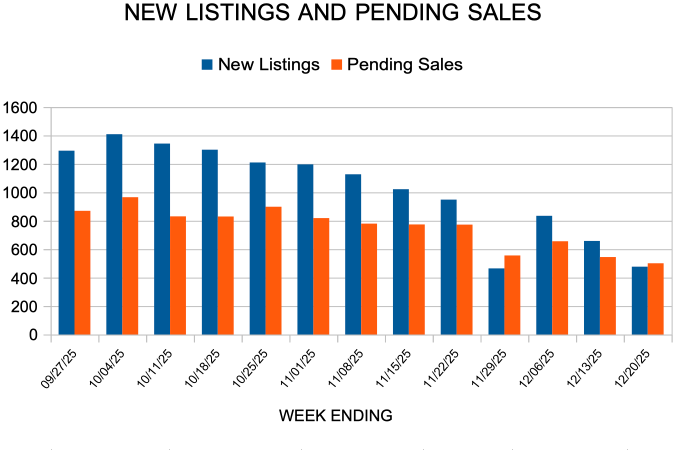

January 5, 2026 by

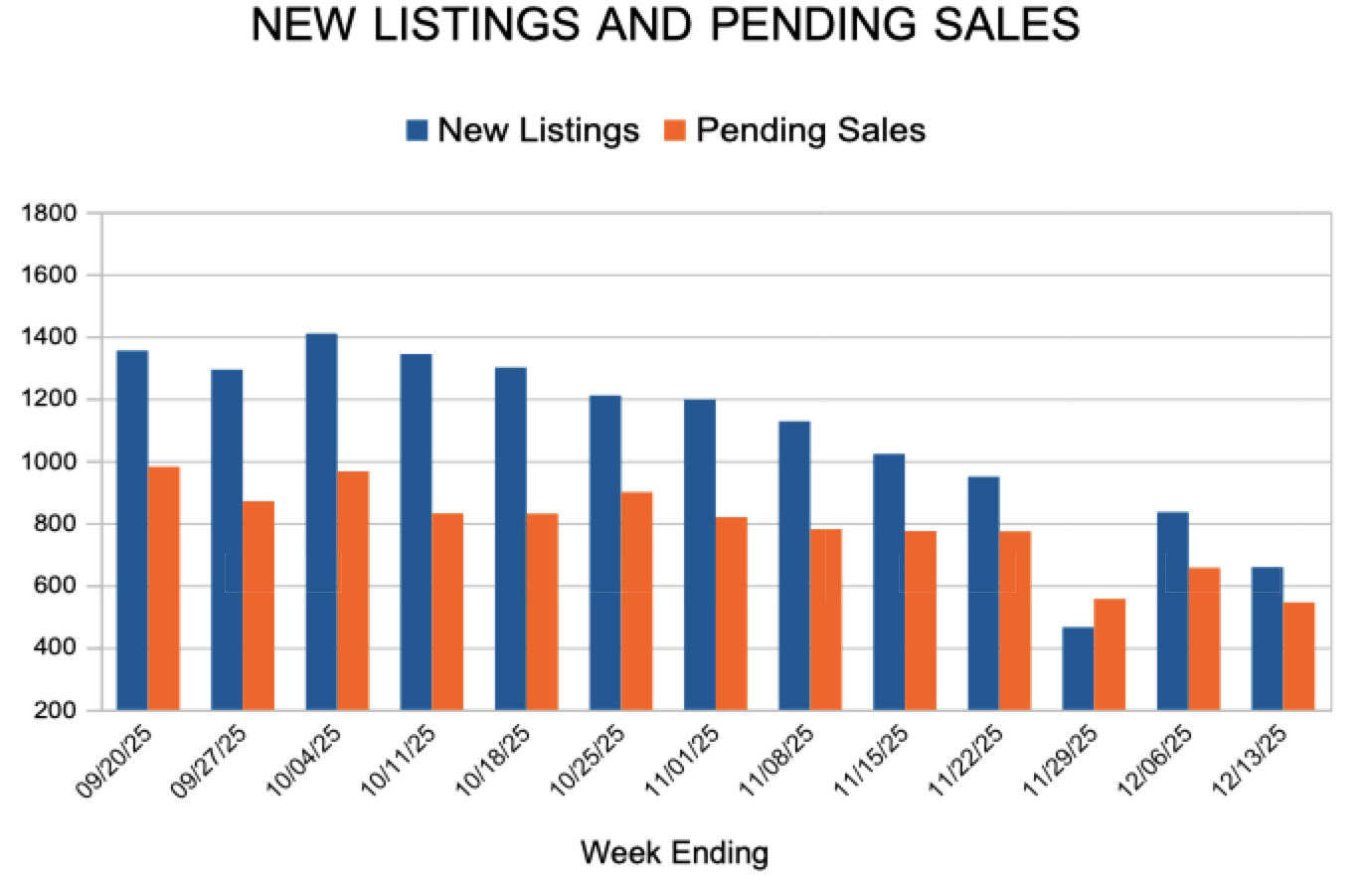

December 29, 2025 by

December 22, 2025 by

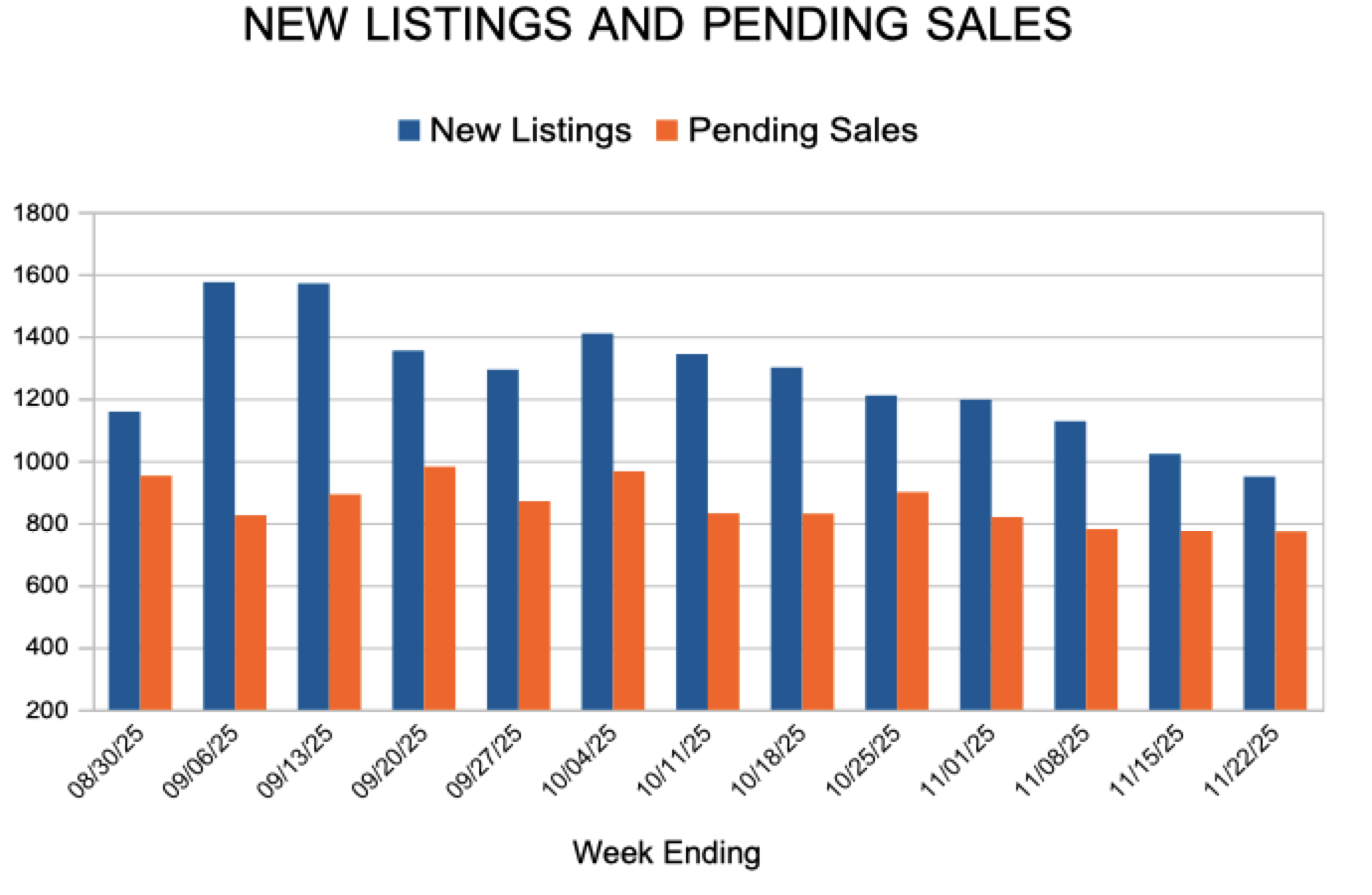

December 15, 2025 by

December 9, 2025 by Mighty Agent

December 2, 2025 by Mighty Agent

November 24, 2025 by Mighty Agent

November 17, 2025 by Mighty Agent

November 10, 2025 by Mighty Agent