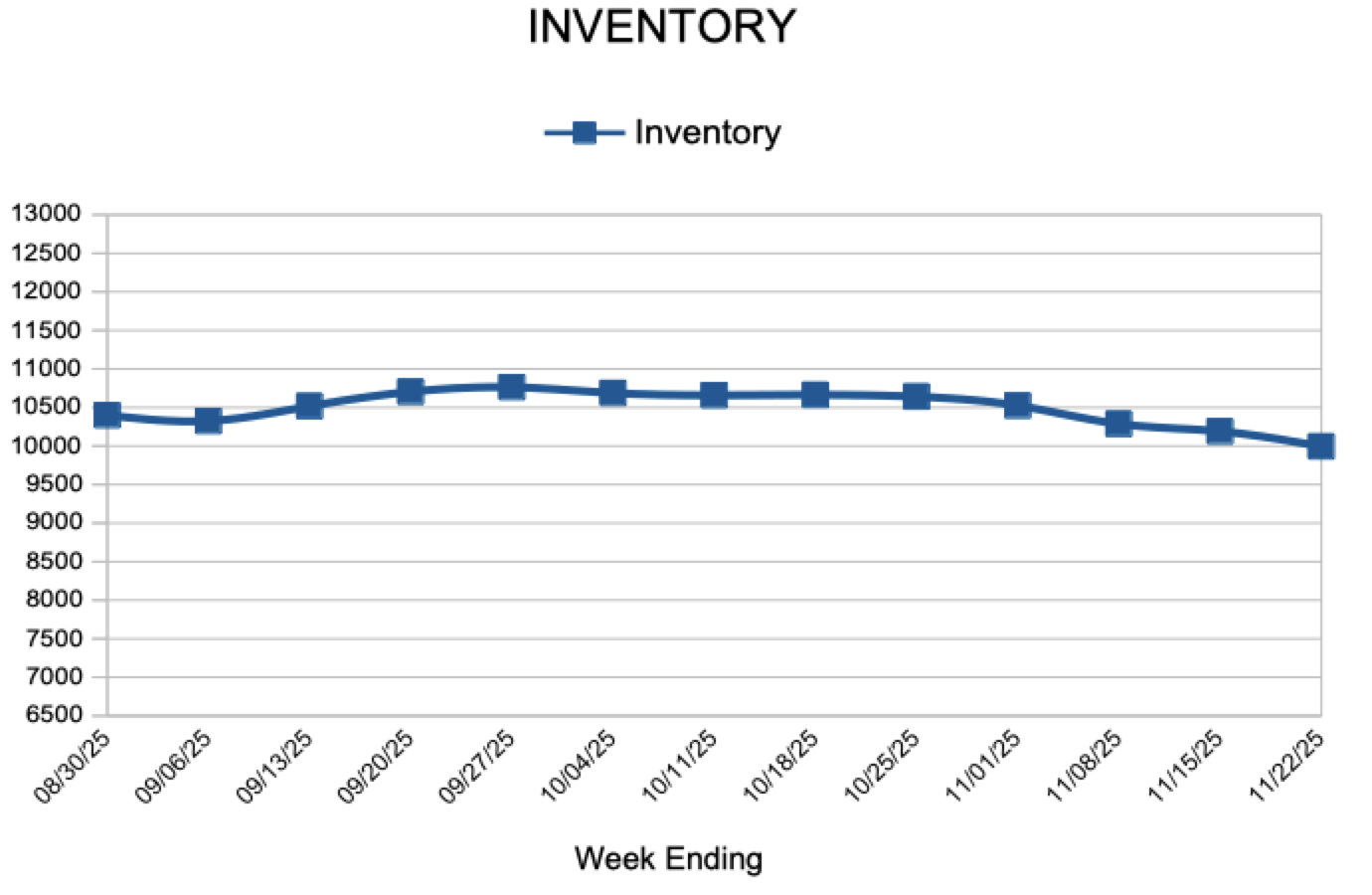

Inventory

For Week Ending November 22, 2025

For Week Ending November 22, 2025

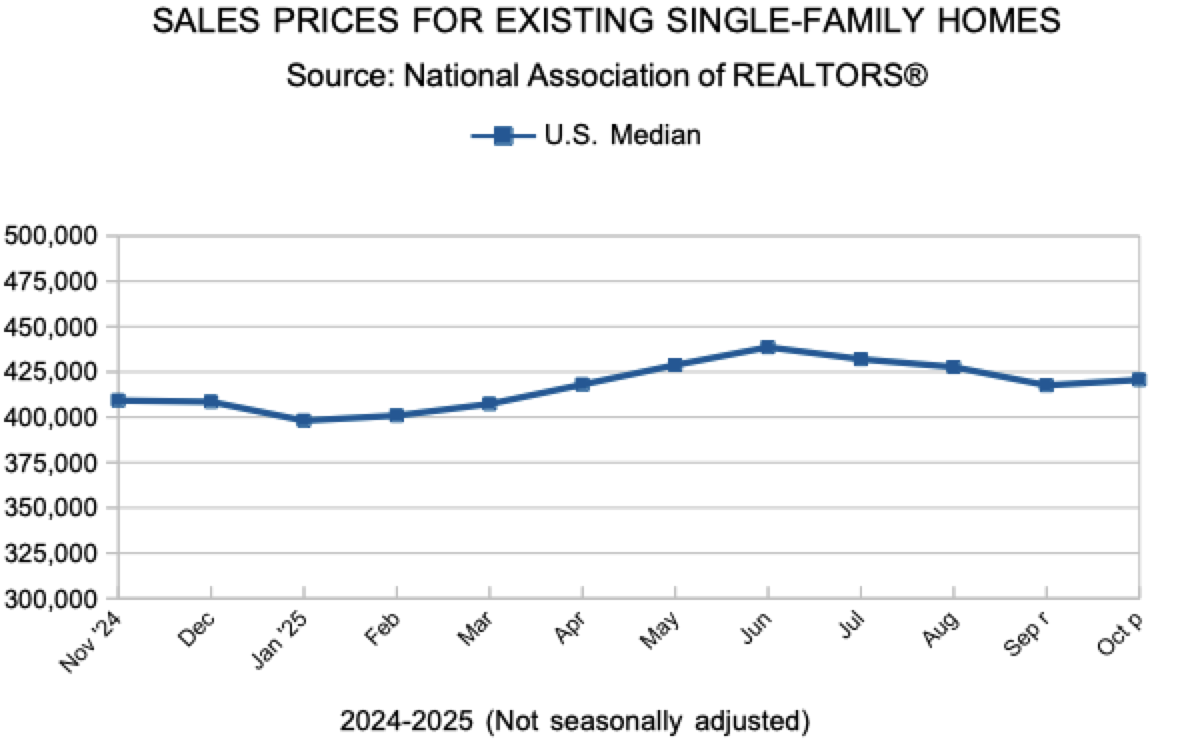

Nearly one-third (32.8%) of all homes sold in the first half of 2025 were paid for in cash, down 0.6% from the same period last year, according to a recent report from Realtor®.com. Cash sales were most common at the low and high ends of the price spectrum and vary across regions, with lower-priced and second-home markets often seeing more all-cash transactions than other areas.

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING NOVEMBER 22:

FOR THE MONTH OF OCTOBER:

All comparisons are to 2024

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

November 26, 2025

Heading into the Thanksgiving holiday, mortgage rates decreased. With pending home sales at the highest level since last November, homebuyer activity continues to show resilience nearing year end.

Information provided by Freddie Mac.

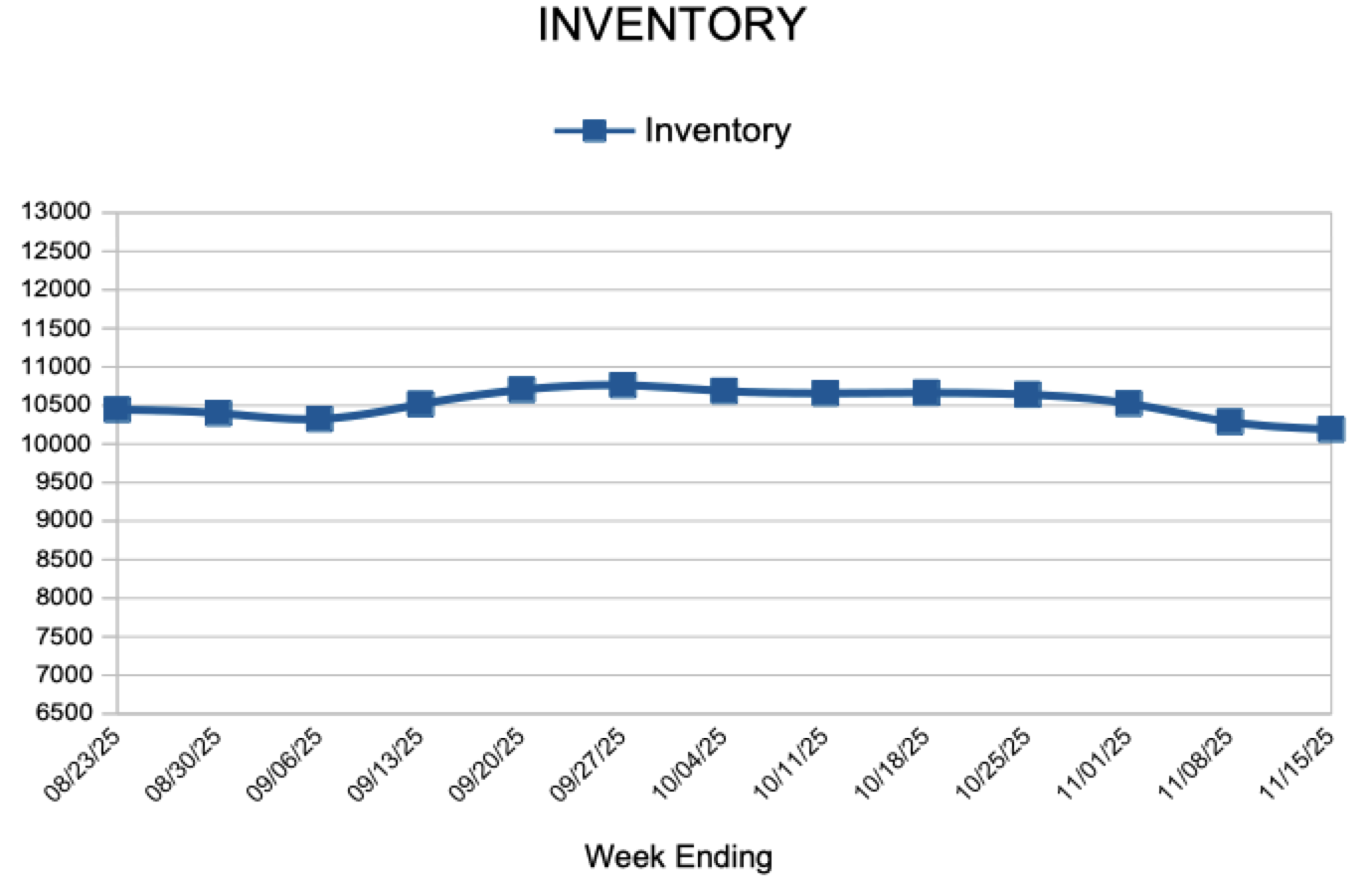

For Week Ending November 15, 2025

For Week Ending November 15, 2025

The U.S. housing supply gap reached 3.8 million units in 2024, according to an analysis by Realtor®.com. For the first time since 2016, new construction outpaced household formations, with more than 1.6 million units completed last year, the highest level in nearly two decades. While builders are making progress, it would still take about 7.5 years to close the housing gap at the 2024 pace of construction.

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING NOVEMBER 15:

FOR THE MONTH OF OCTOBER:

All comparisons are to 2024

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

November 20, 2025

Mortgage rates have been shifting within a narrow ten-basis point range over the last month. This rate stability is a positive sign for both buyers and sellers, as it helps provide greater certainty in the housing markets.

Information provided by Freddie Mac.

Greet me and meet me on social media. You can follow my new listings and changes in the marketplace on any of the following.

Follow me.